Blockchain

Blockchain Technology in Financial Institutions and Banking

The financial system has evolved from analyzing traditional ledgers to providing digital solutions such as online banking and mobile applications. It is not surprising that commercial banks around the world are entering the race for the latest technology in vogue: Blockchain. Financial institutions are increasingly betting on this technology to revolutionize the financial system once again.

Banks and financial institutions are so interested in blockchain the lies of the banking system’s competitive nature and the growing demand for faster and more efficient service. To keep pace with society, which increasingly seeks to see its needs met instantly, financial institutions seek to adapt to the demand for greater agility, new products, and services. However, the sector’s own needs, such as security, continue to be a priority and a challenge in the face of the threat of cybersecurity and hacking.

What is blockchain?

The blockchain is often described as a decentralized ledger or a replicated database on a peer-to-peer network. In other words, this technology is essentially a new type of storage that allows all of its users to share a database and make modifications safely.

Unlike other more traditional options, the data has been duplicated thousands of times through a decentralized computer network (the peer-to-peer network ) independently in this storage system.

With this public and decentralized network, transactions are protected and carried out under a total privacy blanket. Data protection is achieved through the encryption of information in the transaction link. These transactions are based on digital accounts or wallets that grant participants anonymity through their digital identity.

The system works under the participants’ consensus, conditional on each version of the data corresponding in its entirety with the information shared in the database. This eliminates the need for a central authority and puts the control in the participants’ hands, which means that any inappropriate modifications to the database will be immediately detected by all participants, turning this process into an immutable auditing mechanism.

Blockchain technology, also known as the blockchain, was developed as an underlying technology of bitcoin that aimed to record and verify the cryptocurrency transactions. The blockchain has achieved its own place thanks to its potential as a disruptor of the centralized system and streamlined more complex processes. Although bitcoin’s evolution has been erratic, other cryptocurrencies are also gaining attention thanks to this technology and the advantages it offers. To stay updated with blockchain and cryptocurrency news you can find relevant content here.

Blockchain can achieve this thanks to the nature of its design: a collection of distributed, shared, secure and immutable blocks. Each block of information is distributed to all the participants (nodes) in the network, which guarantees a replica to prevent data’s undue alteration. For a transaction to occur, its validity will have to be verified by each of the network nodes, and the information will be registered and shared transparently within the chain.

This is what makes blockchain attractive to financial institutions. To understand how blockchain will fit the modern world’s needs, it is worth taking a step back and analyzing the relevance of this technology in various sectors of the economy.

Who is using blockchain?

The World Economic Forum estimates that the blockchain stores only about 0.025% of the world’s GDP. However, the expectation is that this figure will increase, with banks, insurance companies, and companies in the technology sector leading the trend.

According to research in PwC’s 2018 Global Blockchain Survey, approximately 84% of the executives surveyed are looking to calculate the impact this technology could have on their businesses. At the same time, global companies such as Amazon, Microsoft, IBM, and Facebook are evaluating possible applications for the blockchain, as well as other financial institutions, such as JP Morgan and HSBC, and other leading multinational companies in consulting and audits, such as Accenture and Deloitte (respectively).

The interest that blockchain technology has generated can be observed in the economy’s various sectors, from finance to health and pharmaceuticals. However, banks are leading the advances in the development and implementation of this technology.

Another example is emerging economies seeking the benefits that blockchain technology offers. Kenya has explored the possibility of providing election results in real-time to build confidence in its electoral process. Meanwhile, Nigeria has adopted Oracle Blockchain Cloud Service in its customs services to support merchandise tracking, automate processes, and increase levels of transparency and trust in the business sector.

Among the advanced economies, Spain seeks to apply the blockchain in the forestry sector for time certification and improve the management of logistics companies’ supply chains. Also, in our country, Valenciaport seeks the application of blockchain technology to get closer to the concept of the smart port.

The use of blockchain in banking

For banking, the blockchain’s use offers potential benefits for the prevention of fraud and even for the elimination of some errors typical of humans. On the technical side, the validation, protection, coding, distribution, and tracking of data and transactions are the main attractions of this technology. The blockchain is already considered a transformative agent for settlement and clearing, international transactions, trade finance, identity verification, and loan management.

Since international regulations do not restrict blockchain technology, its implementation has the potential to transform the banking sector and turn it into a cooperative industry between financial services institutions and Fintech companies and boost digital cooperation and innovation. , the evolution of new business models, and more competitive banking.

Spanish banks and the blockchain

Spain quickly recognized the potential of blockchain, and banks are showing a growing interest in this technology. Below, we present some examples of the advances of Spanish banking based on the blockchain:

In April 2018, Banco Bilbao Vizcaya Argentaria issued the world’s first corporate loan with Indra. The transaction of 75 million euros was carried out with its solution based on blockchain technology. In June, BBVA and Repsol closed the first operation of a credit line for 325 million euros, again through its blockchain network. A month later, the bank issued a 100 million euro corporate bilateral loan for the ACS Group.

Banco Santander and leading company Broadridge Financial Solutions used blockchain technology in March 2018 to vote at a general shareholders meeting. Also, Santander launched via iTunes Pay FX, the world’s first application for international payments (Eurozone and USA) based on this technology. In the same year, the bank created a blockchain research team to explore its potential in securities trading, including derivatives, debt, and other products.

In that sense, according to Carlos Bernal, Indra’s director of financial services in the country, the blockchain should stop being seen as a threat, to be seen as an opportunity.

How has the financial sector changed?

It is facing a profound change in the model as a consequence of the digital transformation. Phenomena such as platformization, open banking, or the growing demand for advanced digital identity solutions mark this evolution.

However, rather than as a threat, digital transformation should be a fantastic opportunity to improve entities’ cost structure and increase their predictive capacity in terms of risk analysis.

What is the relationship that the financial sector has with technology?

This sector is in the post smartphone era, which requires the creation of a new model of digital relationship with customers and, for this, it is necessary to evolve from a branch centric concept to another customer-centric, and this is not only achieved with the closure of offices and reduction of staff.

How is security approached within the new financial environment?

The digital transaction is one of the processes that best characterizes the new model towards which the bank is heading. That is why the so-called digital identity is presented as a fundamental technology to implement new business models that take advantage of the digital field’s potential.

What is Indra’s role in this sector?

Indra is a leader in the development of technologies for the financial sector in Spain and Latin America. Currently, the top 10 Spanish entities are clients of the company, and it’s Latin American clients represent more than 40% of total banking assets in the region.

The company manages more than 2,000 projects per year for 400 banking and insurance groups in Europe, Latin America, and the Asia Pacific. And it is the leading company in means of payment in the Iberian Peninsula and one of the largest global operators in Latin America.

Additionally, it is a leading operator in digital transformation, whose differential offering aims to achieve immediate and tangible results.

They recently announced their ability to launch 100% digital banking.

We have an innovative, disruptive, and differential offer that allows creating a native digital bank from scratch in record time. In practice, our model enables the financial institution to respond quickly to the challenges posed by the new context, characterized by an unprecedented level of interaction with customers through exclusively digital channels.

What do banks gain from this?

The banks, which count on Indra as a technological partner, enjoy the highest functionality and ability to serve their customers, thus offering a differential service with high added value.

Thus, the banking customer benefits from a personalized and homogeneous user experience.

What is your perspective on the ‘blockchain’?

For us, this technology has a great capacity for transformation in complex scenarios and processes. Several actors have to trust and collaborate since it provides two essential elements for change: more trust and less friction while focusing on information privacy and performance.

How could the ‘blockchain’ boost the financial sector?

This technology can represent significant savings in terms of infrastructure and an improvement in the efficiency of the processes in the back office.

Besides, it is a facilitator for the development of new digital businesses, which lead to the implementation of new business models and the design of new products and services. The blockchain system works like a large ledger or database.

Do you already have experience in this type of technological development?

BBVA and Indra have successfully concluded the first operation that facilitates the negotiation and signing of a corporate loan using blockchain worldwide; this, in line with their close collaboration to transfer the advantages of the most advanced technology to business operations.

How does blockchain technology help in the accounting of people and companies?

One way that the blockchain can represent a step beyond accounting lies in the fact that, instead of keeping separate records based on transaction receipts, parties will be able to write their transactions directly to a common record. These entries are protected with encryption so that falsifying or deleting them is practically impossible.

Will digital accounting be more and more a trend?

Indeed, the blockchain allows us to go beyond digital accounting. Although digitized, the accounting processes always required a neutral mediator to verify the acceptance of the terms of both parties, making the operation possible.

What other uses does the ‘blockchain’ have?

Despite the advances of the blockchain, financial transactions continue to transit mainly through networks and infrastructures that were built half a century ago. The operating systems of banks were designed on network protocols that are not current.

Therefore, it is not plausible that replacing banking and interbank infrastructures from off-blockchain to on-blockchain is imminent, but it should be intensified as of 2020.

But if a bank uses blockchain, there are no risks that the copy of the database on my computer can be compromised?

Blockchains can be public or private databases. If we had a public registry like a property registry, maybe we would like to have a public blockchain. If we are a private entity, we can choose to encrypt the database, and the encryption system is protected by the collective power of the connected computers. To this day, the world does not know a safer protection system than BlockChain. In a public BlockChain, such as Bitcoin, you can see the history of the transactions, but the two parties’ entity is secret.

In addition to security, Bitcoin offers other benefits. Since each piece of information has a unique identifier, a user’s ability to “double pay” is eliminated. In other words, if I have a digital photo and I send it to my friend, in the world of Bitcoin, the photo cannot be copied, and it is transferred from me to my friend. Bitcoin also offers to speed up transactions and lower costs by eliminating the burdensome part of verifying transactions. Electronic money, financial products, even physical property, can be registered in a BlockChain, eliminating the need for many red tape and lawsuits to determine who is the “real” owner of something.

As a new technology, BlockChain is still being tested and explored to determine its best uses. As JPMorgan Chase and Goldman Sachs, along with bags as NASDAQ, banks are investigated the potential of BlockChain (a technology whose source code is free and available for anyone to download person). In short, BlockChain could represent the next wave of innovation in the financial sector. Is your bank considering how to use it? What other uses could we give to BlockChain? Leave your ideas in the comments section.

Blockchain

5 Reasons Why Delta Exchange is the Easiest Platform for Crypto Trading Strategies in the Indian Market

Crypto trading in India has grown exponentially in the last few years. In 2025, the market pulled in $258 million in revenue and is on track to hit nearly $732 million by 2033, growing at a 14.3% CAGR from 2026 onwards. That kind of money doesn’t come from people buying Bitcoin on a whim and hoping for a lucky spike. It comes from traders who plan entries, manage exits, build hedges, and run full-blown crypto trading setups.

This shift has created a new problem. Most Indian crypto exchange apps still feel built for basic spot buying without any advanced features to try. You open five tabs, check prices on one app, place orders on another, track risk on a third, and hope nothing slips through.

Delta Exchange transforms the story here. Instead of spots, Delta offers a safe trading platform to explore crypto derivatives (futures and options) across major currencies.

Let’s understand more about Delta Exchange and why so many Indian traders end up sticking with it once they try it.

Why Try Crypto Trading Strategies on Delta Exchange

Ranked among the top Indian crypto exchanges, Delta Exchange offers a range of features and analytics tools to simplify your crypto trading experience.

Here’s why many traders trust Delta Exchange:

- INR trading keeps things simple

If you’ve ever had to convert INR to USDT or USD just to trade Bitcoin, you know the hassle. Delta Exchange lets you deposit and withdraw in INR directly via UPI, IMPS, NEFT, and bank transfer, with your margin and profits shown in INR.

That means no awkward crypto conversions or extra wallets – you fund your account straight from your bank and start crypto trading like it’s normal money.

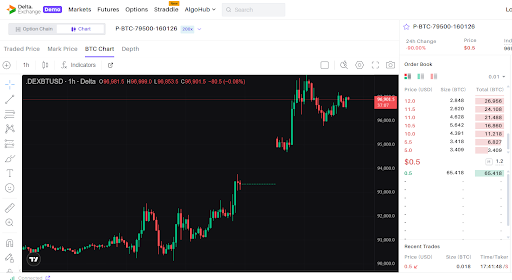

- Algo trading bots that actually work

Automation can save hours and reduce emotional stress and decisions, especially with fast moves in crypto F&O. Delta Exchange supports algo trading through APIs and bot integrations from platforms like TradingView and Tradetron.

You can link your trading strategy to webhooks or APIs and let bots place trades for Bitcoin futures or other crypto options even when you’re away. If you want systematic, repeatable strategies with fewer missed opportunities, this setup feels practical and real.

And the best part? You don’t need to have any coding knowledge or degree – API Copilot does it all for you.

- Lower trading fees that don’t eat into your wins

Fees matter because every percentage point you pay is one less in your pocket after a winning trade. Delta Exchange offers competitive taker and maker fees, plus a fee cap on options that limits how much you pay on low premium trades.

This helps keep costs predictable, whether you’re trading Bitcoin or ETH futures and options. Traders who place frequent trades or use multi-leg strategies on the Indian crypto exchange can keep more of their gains, rather than having them eaten up by trading fees.

- Strategy Builder for practical trading plans

Strategy planning can get messy if the platform doesn’t help you visualize outcomes. Delta Exchange offers tools that let you craft crypto F&O setups with clear strike choices and expiries, plus daily, weekly, and monthly options for more precise timing. This helps you conveniently plan spreads, straddles, or hedges.

- Compliance and risk measures to know

It’s one thing to trade, another to trust the platform doing it. Delta Exchange is registered with India’s Financial Intelligence Unit (FIU) and follows local KYC and AML rules.

For risk management, the platform supports:

- Margin controls and stop-loss tools that help you manage positions while you trade Bitcoin or other crypto derivatives.

- Demo account to practice trades and understand the market without real money.

- Payoff charts show you how your trade will play out with breakeven points and maximum P&L.

This way, you can study your crypto trading strategy better before finalizing the trade.

Apart from these, Delta also offers leverage up to 200X – a good way to amplify your profits if the market moves in your favor.

The Bottomline

Indian crypto traders have moved far past the buy-and-hold phase. Spot crypto trading still has its place, yet most active users now want faster ways to make money from price swings, not wait months for a rally.

That’s where crypto F&O, spreads, and short-term setups step in. You want tools that let you react within minutes, control risk, and lock gains when the move shows up.

Platforms that only support basic coin buying just can’t keep up with that style of trading. Serious traders want flexibility, speed, and ways to work with volatility, not sit through it – and Delta Exchange caters to such traders well.

Disclaimer: Crypto trading carries inherent risks due to its high volatility. This article is for informational purposes only. Kindly do your own research before making any investment decisions.

Blockchain

MoonExe Aligns With the Next Phase of Stablecoin Payments as Global Regulation Accelerates

MoonExe today reaffirmed its strategic focus on stablecoin-powered payment infrastructure as global regulatory clarity continues to accelerate across major financial jurisdictions.

Regulators worldwide are advancing frameworks that formally recognize stablecoins as legitimate instruments for payment, settlement, and treasury operations. Legislative initiatives in the United States, expanded licensing regimes in Asia, and structured compliance approaches in other regions are collectively signaling a transition from experimental adoption to regulated, real-world deployment.

As stablecoins move deeper into mainstream financial infrastructure, demand is increasing for platforms capable of delivering real-time liquidity, transparent pricing, and verifiable settlement. MoonExe’s Exchange Finance (ExFi) model is designed to address these needs by enabling stablecoin-based currency conversions that operate continuously, without dependence on traditional banking cut-off times or geographic limitations.

The platform focuses on facilitating efficient value movement while maintaining transparency through public blockchain records. Transactions executed within the MoonExe ecosystem can be independently verified via standard blockchain explorers, reinforcing confidence through auditable, immutable data.

In parallel with regulatory progress, market participants are increasingly prioritizing infrastructure reliability over speculative activity. Stablecoins are being evaluated less as alternative assets and more as operational tools capable of supporting cross-border payments, digital commerce, and treasury flows.

MoonExe continues to expand its infrastructure and partnerships to support this evolution, positioning itself as part of the foundational layer required for stablecoins to function at global scale.

For more information about MoonExe and its stablecoin payment infrastructure, visit https://moonexe.com/

Blockchain

Playmaker to Launch in Q2 2026 as Midas Labs Expands Its AI-Powered Game Creation Ecosystem

Midas Labs, a UK-based Web3 technology company, has announced the upcoming launch of Playmaker, an AI-powered game creation and launchpad platform scheduled for Q2 2026. The platform is designed to lower barriers to game development and funding, operating as a core product within the UNIFI-powered Midas ecosystem.

Playmaker will provide creators, indie studios, and early-stage visionaries with an integrated environment to ideate, build, fund, and publish games without the traditional constraints of large teams or complex technical infrastructure. By combining AI-assisted creation tools with a structured launchpad and marketplace, the platform aims to streamline the path from concept to live product.

According to Jonathan Wheatley, Chief Marketing Officer of Midas Labs, Playmaker represents a natural progression of the company’s ecosystem strategy.

“Playmaker is about enabling participation at every level — from creators and developers to early supporters and players,” said Wheatley. “By integrating AI-driven creation with funding and publishing infrastructure, we’re building a system that allows ideas to move efficiently from concept to execution.”

The platform is powered by the $PLAY token, a fixed-supply utility asset used for project participation, creator payments, marketplace transactions, and ecosystem services. $PLAY operates within the broader UNIFI ecosystem, where UNIFI serves as the access and conversion layer, reinforcing liquidity and alignment across Midas Labs’ products.

Midas Labs has structured Playmaker’s token economy around a non-mintable, scarcity-driven model, designed to support long-term sustainability as platform adoption increases.

The Playmaker launch builds on recent Midas Labs milestones, including the expansion of the Midas Play Marketplace, multiple game releases, ecosystem partnerships, and the rollout of UNIFI staking infrastructure. Together, these components form a vertically integrated environment linking creation, funding, distribution, and participation.

Playmaker is scheduled to go live in Q2 2026, with phased ecosystem access beginning with early contributors before expanding globally.

About Midas Labs

Midas Labs is a United Kingdom–based Web3 technology company focused on building scalable digital ecosystems across gaming, AI, and creator-driven platforms. Powered by the UNIFI token, Midas Labs develops infrastructure designed for long-term participation, real utility, and sustainable growth.

New AI cybercrime tool breaches banking KYC systems using advanced deepfake technology

Bitfire Group Joins Hong Kong Web3 Festival as Diamond Sponsor

ZA Bank Confirms Participation at Hong Kong Web3 Festival

AltLayer Announced as Gold Sponsor for Hong Kong Web3 Festival 2026

Conflux Joins Hong Kong Web3 Festival as Secondary Exhibition Sponsor

Web3 Leader Programme is an official Platinum Sponsor at Hong Kong Web3 Festival 2026

Cardalonia Aiming To Become The Biggest Metaverse Project On Cardano

P2P2C BREAKTHROUGH CREATES A CONNECTION BETWEEN ETM TOKEN AND THE SUPER PROFITABLE MARKET

WOM Protocol partners with CoinPayments, the world’s largest cryptocurrency payments processor

ETHERSMART DEVELOPER’S VISION MADE FINTECH COMPANY BECOME DUBAI’S TOP DIGITAL BANK

Project Quantum – Decentralised AAA Gaming

WOM Protocol Recommended by Premier Crypto Analyst as only full featured project for August

-

Crypto4 years ago

Crypto4 years agoCardalonia Aiming To Become The Biggest Metaverse Project On Cardano

-

Press Release5 years ago

Press Release5 years agoP2P2C BREAKTHROUGH CREATES A CONNECTION BETWEEN ETM TOKEN AND THE SUPER PROFITABLE MARKET

-

Blockchain6 years ago

Blockchain6 years agoWOM Protocol partners with CoinPayments, the world’s largest cryptocurrency payments processor

-

Press Release5 years ago

Press Release5 years agoETHERSMART DEVELOPER’S VISION MADE FINTECH COMPANY BECOME DUBAI’S TOP DIGITAL BANK

-

Press Release5 years ago

Press Release5 years agoProject Quantum – Decentralised AAA Gaming

-

Blockchain6 years ago

Blockchain6 years agoWOM Protocol Recommended by Premier Crypto Analyst as only full featured project for August

-

Press Release5 years ago

Press Release5 years agoETHERSMART DEVELOPER’S VISION MADE FINTECH COMPANY BECOME DUBAI’S TOP DIGITAL BANK

-

Blockchain6 years ago

Blockchain6 years ago1.5 Times More Bitcoin is purchased by Grayscale Than Daily Mined Coins